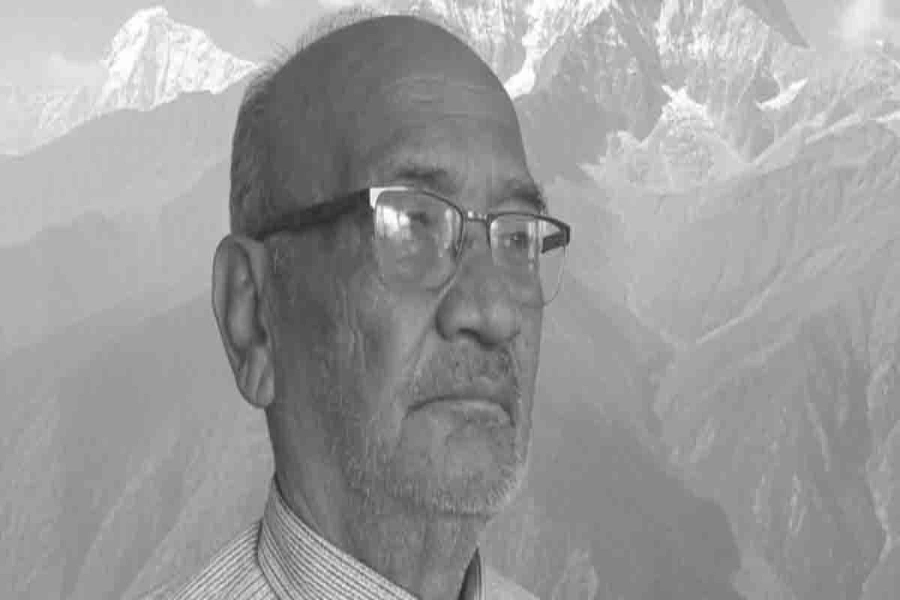

Bhuvan Kumar Dahal took charge of Sanima Bank Ltd as its CEO in January 2014. The bank promoted by non-resident Nepalis (NRNs) is best known for its lowest level of bad loans, balanced rise in business volume, dominance of young faces in the management, and adoption of modern banking technologies.

Revised interest rate corridor system introduced

Unlike other banks which are feeling pressure to raise paid-up capital to Rs 8 billion within two years through merger and acquisition, Sanima Bank has announced an 'organic growth' through bonus and rights issue. With two and half decades of experience in banking industry, Dahal is credited for bringing the youngest commercial bank to the Top 10 list as per CAMEL rating last year. Sagar Ghimire of Republica talked to Dahal on wide range of issues related to banking industry. Excerpts:

Looking at financial results of the 2nd quarter, it seems that banking industry is left untouched by excess liquidity, devastating earthquake, Tarai turmoil and Indian blockade. Can we conclude that banks weathered all the crises?It has impacted every borrower, but not to an extent that they cannot service their debt. The impacts are largely limited to few sectors like tourism, construction and some areas. Many businesses are not operating at full capacity due to rise in operating cost which ultimately passes on consumers. Since there is not much business transaction in festival season, Kartik (mid-October to mid-November) was less-affected despite strike and blockade. While Mangshir (mid-November to mid-December) was highly affected, supply relatively eased in Poush (mid-December to mid-January), keeping the economy afloat. Also, foreign employment continued to send money into the country. The impact became less visible also due to the recent relaxations offered by Nepal Rastra Bank (NRB).

What about the impact of excess liquidity?

While there was liquidity crunch in the banking system until mid-June 2013, there was a surplus in 2014. Again there was crunch for few months in 2015. Before the April earthquake, the liquidity crunch had driven up the fixed deposit interest rates to 8 percent. Thus, liquidity is in a seesaw trend. What is true is there is always a surplus situation in the funds that banks make investment in the government securities due to Credit Deposit Ratio requirement. The return on government securities has always remained in a lower side in the last five years.

Lending rates have not gone down on par with deposit rates. Why are banks reluctant to offer more interest to depositors, or charge low interest to borrowers?

The return on government securities and central bank instruments is below one percent which is terribly low compared to inflation rate. Banks have parked around Rs 130 billion in central bank instruments which they would have lend had there been demand. If you talk about Sanima Bank, we are offering up to 4.5 percent interest rate on saving deposit while many have brought it down to the range of around 1 to 3 percent. I am parking the money that I buy at 4.5 percent from depositors in the central bank instruments at below 1 percent. I compensate the shortfall between deposit and investment returns through my borrowers. If the government has borrowed with us at a reasonable rate, we would have been compelled to reduce the loan rate for borrowers. Despite this, almost all banks have interest spread below 5 percent. One of the major reasons behind banks not reducing rates significantly is due to negligible return that they get in government securities.

Do you see the risks of rise in speculative investments from the current ultra-low deposit rate scenario?

Such risks cannot be ruled out. It is very unfortunate that the lending rate is much lower than the inflation rate. The inflation is at 11 percent while the big borrowers are getting loans at 6 to 6.5 percent. Even general consumers now get home loans and auto loans at around 7 percent. Those who used to deposit money in the banks might have already been tempted toward speculative investments. A reason behind the recent spectacular growth of stock market might be the ultra-low interest rates on deposit. There are also chances of rise in real estate prices in the near future if this scenario persists.

Many criticize recent central bank's relaxations to the borrowers battered by earthquake and other problems will only cover up their wounds. What do you say?

Personally, I had also requested the central bank that the debt servicing, which is overdue more than 90 days, should be categorized under 'watch' list with 5 percent loan loss provision instead of retaining it under 'pass' category with 1 percent loan loss provision. Let's hope it will not have painful impact for the banks.

Sanima Bank has announced capital increment plan by issuing rights and bonus shares to meet capital increment diktat by NRB. Don't you think this is going to hit bank's capacity to provide return on equity?

We have pursued an organic growth plan that is likely to impact return on equity. But if you see our growth in last few years, you see it is sustainable. We are increasing around Rs 10 billion of assets every year. Even after we raise capital to Rs 8 billion, there will be surplus fund only for around two years. It is a pleasant fact that we, the youngest bank, is in the Top 10 club. Though the return on equity may not be at the current level, it will not be terribly low. We have cautiously planned the capital growth to increase our assets so that it does not strain our return on equity.

Why are bankers opposing a provision in BAFIA amendment that bars CEO and chairman from holding their post for more than two terms?

If the chief executive wants to do something in an institution, two terms, or eight years, is adequate for him/her. You can prove your mettle during that time. Regarding two-term limit for chairperson, I think it is a prudent move toward corporate governance. However, this is my personal opinion.

Sanima Bank's unique feature is its lowest level of nonperforming loans (NPL). How have you managed to contain bad debts to such a negligible ratio?

Sanima Bank has been very conservative in terms of assessment of risk while floating loans. Our Business Unit recommends loan proposal which must be approved by Risk Unit. Even I, the CEO, cannot do anything if the Risk Unit rejects the loan proposal. The bank is striking a delicate balance between the Business Unit that has a business target and Risk Unit which is mandated to contain NPL to a certain level. We have created five to six layers while approving loans so that one or another will flag the risks even if it slips through the crack. We also make tremendous efforts on follow-up of loans repayment.

Sanima Bank is promoted by NRNs. What international values have they brought to your institution?

Our promoters bring the experience of having worked in Europe. They are absolutely committed toward a professional culture where day-to-day operation of a bank is run by the management and control of policy by the board. None of our employee is related to our board directors, promoters with controlling stake or management. NRNs suggest us to follow best practices they see abroad but they do not impose their wills on day-to-day operation.