Sunday, 28 April 2024 01:02 PM

OR

Login using

Opinion

Environmental and Social Risk Management in Nepali Banking: Policy, Implementation and Status

Published On: September 30, 2023 08:30 AM NPT By: Anil Kumar Jha

Anil Kumar Jha

The author is an Assistant Director at Nepal Rastra Bank. He is also a PhD scholar in Regulation and Supervision of Nepalese Banking Industry at Tribhuvan University.news@myrepublica.com

Central banks as regulators are responsible for providing support and guidance to regulate banks and financial institutions (BFIs) for the development and execution of Environmental and Social Risk Management (ESRM) guidelines. This in turn helps improve risk management practices by integrating Environmental and Social Risks. The future of sustainable banking industries depends on the ability of banks to identify and manage environment/climate and social risk.

The focus of emerging and developing countries to seek a “green economy” has enhanced the importance of ESRM for regulators as well as the banking industry. Hence, ESRM is not only the concern of the central bank and BFIs but also the concern of the national economy. ESRM is a framework that assists lending organizations to identify, assess, and mitigate the potential financial impacts of environmental and social risk. Though BFIs have been managing several other types of risks in their organization, environmental and social risk management is still at an early stage of development. The successful implementation of ESRM in any country requires holistic approach of regulators and BFIs and well-conceived and coordinated actions of various stakeholders who need to implement ESRM.

One on side, there is growing importance of ESRM in banking industries, while on the other side there is a debate as to whether or not BFIs should invest their resources to implement ESRM and whether it will create value for the shareholders or not. Another important issue is whether implementing ESRM will slow down loan processing and reduce business opportunities of BFIs or not. Many studies and research carried out in different parts of the world to understand the linkage between performance of banking institutions and implementation of ESRM found evidence suggesting that there is direct and positive linkage between implementing ESRM and performance of BFIs. Implementing ESRM is found to be beneficial for improving the quality of credit portfolio, improving brand value and reputation of BFIs, increasing long-term business opportunities and competitiveness, and providing sustainability to BFIs.

Policy Guidance

The Alliance for Financial Inclusion (AFI), which is a policy leadership alliance jointly owned by central banks and other regulatory institutions to regulate financial sector of 82 member countries with common objective of enhancing financial inclusion, has formulated a wide range of policy and regulatory guidance for formulation and implementation of ESRM guideline. The policy guidelines recommended by API are organized into three pillars including Pillar One: The Governance and Strategy Pillar, Pillar Two: The Risk Management Pillar, and Pillar Three: The Disclosure and Stakeholder Management Pillar. Along with these three pillars there are implementation recommendations and role of supervisor after formulations and implementation of ESRM policy.

Under the Pillar One, there are five guiding principles including 1) ESRM is foundation of corporate governance (Shareholders, Board of Directors, and Senior management must understand the issue), 2) ESRM is an issue of strategic importance (should be incorporated in strategic plan and strategic management framework), 3) Implementation of risk based pricing (incorporate ESRM in strategic plan as a source of reward), 4) Communicate expected values and behaviors (top management must communicate importance of ESRM to employees), and 5) Early actions (ESRM discipline will evolve overtime but proactive approach is required).

Similarly, under the Pillar Two, there are another five guiding principles for risk identification, assessment and risk management. ESRM should be considered as sources of both risk and reward as a result, a risk-based approach should be taken by BFIs rather than a compliance-based approach. The five guiding principles of pillar two include: 1) ESRM is part of holistic risk management framework (should be included in risk appetite of BFIs, it is not distinct), 2) ESRM should be implanted in credit risk management culture considering both physical and transition risk (integrating environmental and social data in risk management process), 3) Incorporate ESRM as source of operational, market and liquidity risk, 4) Develop robust and relevant monitoring and reporting system ( develop indicators and ensure timely and consistent reporting), and 5) Include ESRM in scope of internal audit and compliance functions (include ESRM in all three line of defense, internal audit and compliance should cover it in their scope and provide recommendations for improvement).

Likewise, even under the Pillar Three, there are another five principles including: 1) Prepare for the evolving requirement of regulators for disclosure of environmental and social risks (expect inquiries by regulators related with policy, governance and strategy related with ESRM, environmental and social risk management information system, expertise of staff, risk exposure by types, entity, sector, assessment of impact in case of loss, assessment of actual loss or risk), 2) follow and adopt ESRM reporting disclosure recommended by regulators or international corporate, 3) Use ESRM disclosure to build public relation/communication, 4) Justify the ESRM values and behavior to staff through communication, and training and development , and 5) Communicate and support borrowers/customers and provide feedback to them.

Implementation Recommendation

Once ESRM guidelines have been formulated based on the three pillars recommended by API it is the responsibility of regulators and supervisors to support BFIs to implement it. The Alliance for Financial Inclusion, Inclusive Green Finance Working Group (AFI, IGFWG) has recommended some initial implementation for regulators and banking supervisors. These recommendations include: 1) Industry consultation (consulting ESRM guideline with industry, collecting feedback, revision and clarification of guidelines), 2) Sequencing (support BFIs to develop ESRM policy, upgrade risk management system, training for employee, setting appropriate timeline for supervisory), 3) Promotion (exchange of knowledge between borrowers, lenders, regulators and supervisors, government agencies, and other stakeholders through conference, workshop and other events), and 4) Supervision of ESRM Policy (review ESRM implementation during supervision though supervisory review and evaluation Process (SREP) by evaluating potential capital requirement for environmental and social risk, disclosure under pillar three of Basel framework, monitor the potential impact financial inclusion indicators and watch for early warning signs.

For the successful implementation of ESRM, supervisors should consider various activities including communicating with BFIs, ask for the plan with BFIs regarding implementation of ESRM guidelines, collect information regarding status of implementation during onsite-supervision, conducting high level dialogue and programs related with progress, encourage BFIs to cover ESRM in scope of internal, audit and compliance, monitor financial inclusion indicators in context of ESRM policy implementation, continuous analysis of current status and assist BFIs to implement ESRM guidelines.

Status of Nepal

In case of Nepal, Nepal Rastra Bank as a regulator first formulated and published guidelines on “Environmental and Social Risk Management (ESRM) for Banks and Financial Institutions” in May, 2018 setting mandatory regulatory requirements applicable to all banks of Nepal. This guideline was revised in February, 2022. The provision of mandatory reporting started in 2022. This guideline focuses on environmental, climate, and social risk related with the business activities of BFI’s clients and defines scope of applicability to various types of financing including SME, commercial leasing, Working capital financing, term loan and project financing. incorporates ESRM tools, templates, and checklists to assist non-technical staff of BFIs to implement ESRM effectively. Besides, it has also defined the role and responsibilities of organization and various staff and divisions of BFIs for incorporating ESRM in credit risk management policy.

The ESRM guideline 2022 also has provisions related with environment and social risk (E&S) management procedures which consist of necessary steps needed to be taken by BFIs for identification, accessing and management of E&S risk. Based on the provisions and reporting templates provided by ESRM guidelines most commercial banks have started to submit ESRM reports in supervisory information system (SIS) since 2078/79 BS. The reporting templates consist of three parts including 1) Policy formulation and governance, 2) Employee training and capacity building, and 3) Incorporation of environment and social risk in core risk management.

In the policy and governance part, BFIs need to report if ESRM policy as well as procedure/manual has been formulated and approved by BOD with date of approval. They need to report if an ESRM officer has been nominated with the date of nomination. Likewise, in the employee training and capacity building part, BFIs need to report about quarterly funds allocated for ESRM related training, seminar, workshop and other programs, number of such training and programs with number of participants. Similarly, incorporation of E&S risk in core risk management includes quarterly data on the number of loans rejected due to exclusion list, number of transactions subject to E&S due diligence (ESDD), share of ESDD transactions in total loan portfolio, total number and amount of disbursement by E&S risk rating, number of transaction with E&S action plan, number of transactions rejected on E&S background, and number of transaction beneficial to E&S improvement in different five sectors (renewal energy, energy efficiency, wastewater treatment, waste recycling and reuse, and water consumption reduction).

Though commercial banks have started to report ESRM, it is yet to be implied in other lending institutions. Besides, consistency and accuracy of such reports need to be analyzed on a regular basis. The ESRM has not yet been incorporated in SREP. Considering all this, we can say that the progress of Nepal to incorporate ESRM is satisfactory but not sufficient as lots of work is yet to be done especially in implementation, capacity building, reporting, and supervisory. However, since it is a new phenomenon and there are various stakeholders associated with ESRM, successful implementation will take time. As it is a challenging task, we need to learn it by doing. Similarly, we need to understand that implementation of ESRM is not only the sole responsibility of Nepal Rastra Bank. Instead, a joint effort of all stakeholders is necessary for the full implementation of ESRM in the banking sector of Nepal.

You May Like This

Rolpa at high risk of COVID-19 outbreak; doctors anticipate worse situation in the days to come

ROLPA, Nov 30: Health professionals in Rolpa have urged the government to add isolation centers and speed up contact tracing to... Read More...

NRB urges BIFs to contribute for economic development

KATHMANDU, Nov 11: The Nepal Rastra Bank has warned of taking stern action against the bank and financial institutions if they... Read More...

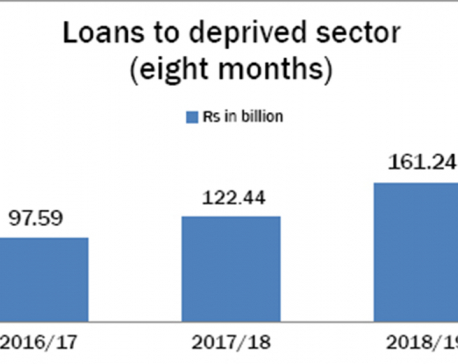

Expansion of network, definition drives up deprived sector lending of BFIs

KATHMANDU, May 12: Bank and financial institutions (BFIs) have floated a total of Rs 161.24 billion in loans to deprived sector... Read More...

-1200x560-wm_20240427144118.jpg)

Hearing on Cricketer Lamichhane’s appeal today

21 minutes ago

Nepal Investment Summit (live)

34 minutes ago

Just In

- President Paudel issues ordinance related to facilitation of investment

- Hearing on Cricketer Lamichhane’s appeal today

- Nepal Investment Summit (live)

- Clear Policies Set to Boost American Investment in Nepal: US Ambassador Thompson

- Second T-20 series: Nepal loses toss, set to go for fielding first

- Nepal Investment Summit 2024 and Victor Hugo Moments for Reforms

- Kathmandu continues to top the chart of world’s most polluted cities

- 3rd Investment Summit: Govt seeking letters of intent for 20 projects

Leave A Comment