Friday, 26 April 2024 06:58 AM

OR

Login using

Liquidity crunch

Halt in lending likely as banks see loan-able funds dry up

Published On: January 25, 2017 01:10 AM NPT By: Sagar Ghimire | @sagarghi

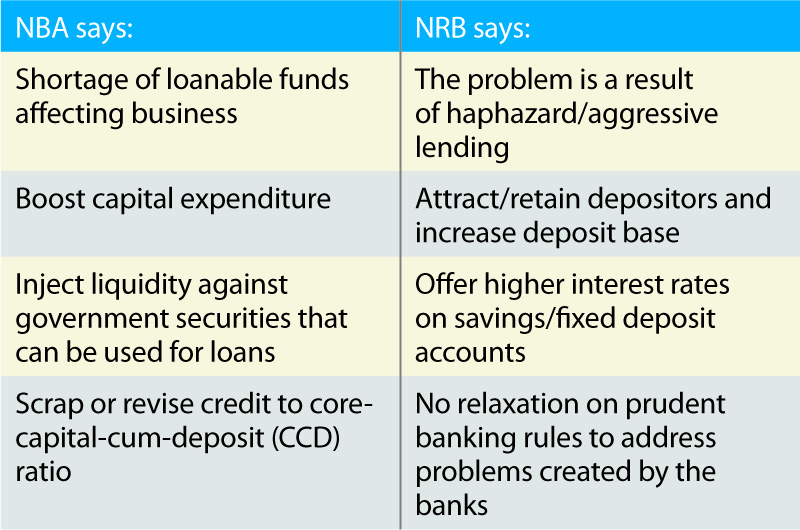

Not our problem, says NRB

KATHMANDU, Jan 25: Commercial banks are literally left without any money to extend new loans, indicating that credit expansion of most of these banks will come to a grinding halt if they do not receive fresh financing facility.

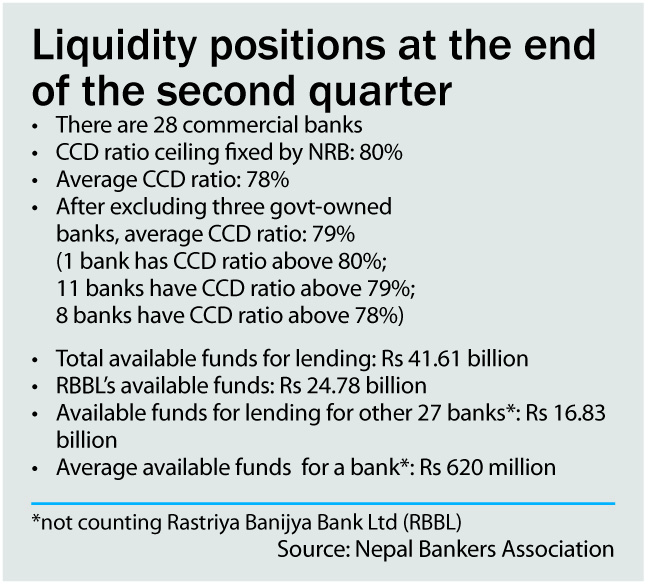

According to figures released by Nepal Bankers Association (NBA), the umbrella organization of 28 commercial banks of the country, commercial banks have a combined Rs 41.61 billion left for lending. Out of this, Rastriya Banijya Bank Ltd (RBBL) -- a government-owned bank -- holds Rs 24.78 billion, while remaining 27 commercial banks have only Rs 16.83 billion which can be used for credit purpose. Excluding RBBL, a commercial bank has an average of Rs 620 million at its disposal for lending.“

"As this scarce fund should be used for disbursement to borrowers to whom the bank has already pledged, there is no way we can provide loans to new borrowers and projects," Anil K Shah, president of NBA, said.

The liquidity, or loanable fund, crunch is attributed to the sudden surge in the lending despite slowdown in deposit mobilization. Deposits have slowed in recent months due to deceleration in remittance growth as well as the failure of the government to increase development expenditure, while banks have been on a lending spree amid rising credit demands and pressure to expand business with the rise in their paid-up capital. The lethal combination of these two trends has now resulted into shortage of funds which was in abundance in the banking system until the last fiscal year 2015/16.

The government has a treasury surplus of nearly Rs 203 billion as of Sunday, thanks to failure to speed up development spending. Had this surplus fund, which is lying idle in the government, been spent as planned, it would have pumped money into the banking system. Bank deposits depleted further when taxpayers withdrew nearly Rs 40 billion from the banking system to file taxes at the second quarter-end.

Bankers say that the central bank should immediately intervene to insulate the economy from the effect of the liquidity crunch. Either the government should expedite capital spending, which will pump money into the banking system, or the NRB should inject money in the banking system which banks can use as fund for lending against the government securities they hold, according to bankers.“

"Otherwise, the credit to core-capital-cum-deposit (CCD) ratio should be either revised to make it 85 percent or scrapped altogether which will help to free up additional funds in the banking system," Shah, who is also the CEO of Mega Bank Ltd, said. He further said that the provision to maintain 20 percent of net liquid assets to total deposit ratio can govern their liquidity requirement.

The tightening of the CCD ratio -- a rule enforced by the NRB to measure liquidity ratio of the BFIs -- has crippled the capacity of the banks to extend lending. While a bank must have 80 percent of CCD, the average CCD ratio stands at 78 percent, meaning they have only 2 percentage point capacity to lend from the deposits and core capital that they hold. The CCD ratio of a commercial bank is already at 80 percent, while such ration of 11 banks is at 79 percent.

CCD ratio refers to the maximum amount that a bank can extend as loan from its deposit and core capital. For example, if a bank has Rs 100 on deposits and core capital, it can only extend Rs 80 in loans while it has to maintain 20 percent in cash reserve and investment on government securities and cash on their vault.

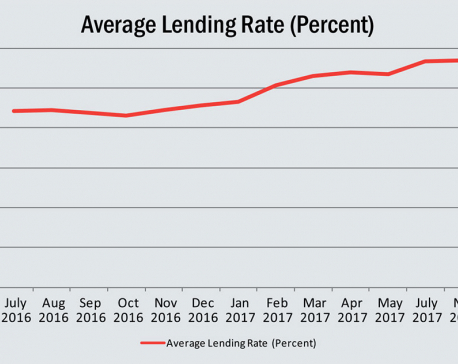

However, NRB seems reluctant to intervene immediately, leaving banks to resolve the problem on their ow“. "This is the problem created by banks themselves through haphazard and aggressive lending without making prudent assessment while floating loans," Narayan Prasad Paudel, an executive director of NRB, told Republica. He advised the banks to offer higher interest rates on saving deposit to attract more funds and retain the deposits that are maturing.“

"Scrapping or relaxing a particular rule to address some problem is against prudential banking norms and practices and financial stability," he maintained.

You May Like This

Banks stop lending amid shortage of funds

Bankers are panicked at the possibility of huge withdrawal of deposits from the system over the next few days for... Read More...

Banks less likely to get foreign currency loans anytime soon

KATHMANDU, May 9: Though Nepal Rastra Bank (NRB) has paved the way for commercial banks for foreign currency borrowing, it seems... Read More...

Credit crunch bedevils banks: Bank deposit rate at 13%, lending rate spikes to 16%

KATHMANDU, Dec 29: Due to lack of farsightedness and aggressive lending practices among banks and financial institutions (BFIs), credit is... Read More...

First meeting of Nepal-China aid projects concludes

17 hours ago

Karnali CM Kandel secures vote of confidence

13 hours ago

Just In

- World Malaria Day: Foreign returnees more susceptible to the vector-borne disease

- MoEST seeks EC’s help in identifying teachers linked to political parties

- 70 community and national forests affected by fire in Parbat till Wednesday

- NEPSE loses 3.24 points, while daily turnover inclines to Rs 2.36 billion

- Pak Embassy awards scholarships to 180 Nepali students

- President Paudel approves mobilization of army personnel for by-elections security

- Bhajang and Ilam by-elections: 69 polling stations classified as ‘highly sensitive’

- Karnali CM Kandel secures vote of confidence

Leave A Comment