Saturday, 27 July 2024 06:26 AM

OR

Login using

Project Syndicate

Contrary to popular belief, world growth hasn’t been especially disappointing so far this decade

I have been out of the world of international finance and economic forecasting for more than four years, but much of what I learned during my 30 years working full-time in the field still influences how I view the world. One lesson was to measure an entity’s economic and financial performance by how it compares both to the entity’s underlying potential and the market’s valuation of its performance.

Applying this approach to the major economies gives rise to some surprising observations—and possibilities.

For starters, contrary to popular belief, world growth hasn’t been especially disappointing so far this decade. From 2010 to 2016, global output rose at an average annual rate of 3.4 percent, according to the International Monetary Fund. That may be lower than the 2000-2010 average, but it is higher than the growth rate in the 1980s and 1990s—decades that are not typically viewed as economically disappointing.

A breakdown of particular countries’ performance offers further insights. Despite significant political trauma, the United States and the United Kingdom have performed as expected. China, India, and Japan have also grown close to their potential. In a rare occurrence, no major economy has dramatically outperformed its potential.

Three economies have, however, genuinely disappointed: Brazil, Russia, and the eurozone. Could that mean that many observers, including me, overestimated these economies’ potential? Or does it reflect extenuating circumstances? If it is the latter, one must ask whether, contrary to prevailing expectations, new developments or shifts in any or all three of these economies might surprise us on the upside for the rest of the decade.

When it comes to the eurozone, embracing the idea that economic growth may be about to take off might be enough, at least until recently, to earn one a referral to a mental-health specialist. But, in my old life, I would be encouraging my analysts to spend more time considering just that possibility, because, on the off-chance that this crackpot notion were true, there would be some serious money to be made in today’s generously valued markets.

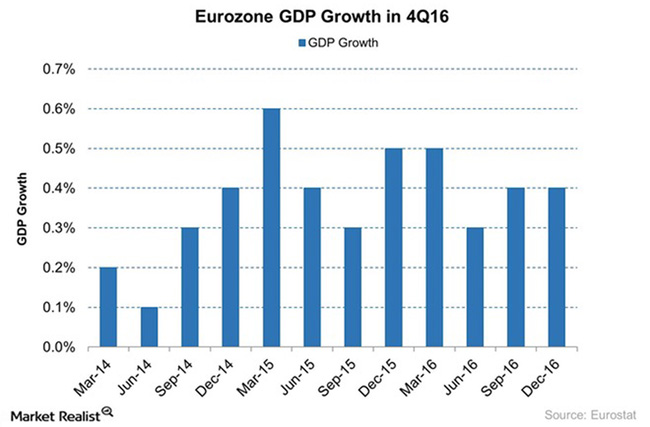

And, in fact, the prospect of a growth pickup in the eurozone might be only partly insane. Cyclically, the eurozone is currently doing well both by its own standards and relative to others. In the first quarter of this year, the eurozone grew more strongly than the US or the UK, and most of the eurozone’s larger countries have been showing stronger relative growth for some time.

Nonetheless, the eurozone’s long-term structural outlook remains uninspiring. The prospects for the two key drivers of long-term growth—the size and growth of the working-age population and productivity—look grim for the eurozone’s largest countries, even Germany, the one economy that most acknowledge is, from a cyclical perspective, doing just fine.

But—to indulge further that outlandish notion of an impending eurozone growth surge—what if something changes significantly to strengthen those growth drivers? With refugees—many of them young—continuing to pour into Europe from troubled parts of the Middle East and Africa, that may not be an altogether fanciful prospect.

Of course, tapping the potential of refugees requires assimilating them to European societies and economies—a challenge that has many Europeans justifiably worried. But, if that need were met, it would certainly mitigate Europe’s mounting demographic challenge, especially in Germany and Italy.

There is also the possibility that new developments will bring about a more constructive policy approach. Most eurozone members’ fiscal positions have undergone considerable, though often unnoticed, improvement in recent years—so much so that the eurozone-wide fiscal deficit is now less than 3 percent of GDP, much better than the US or the UK. Moreover, soaring tax receipts in some parts of the eurozone—notably Germany—are feeding almost embarrassingly large fiscal surpluses. Could now be the moment to push for an ambitious Franco-German-led stimulus effort?

If France’s new president, Emmanuel Macron, manages to obtain sufficient backing in the National Assembly in the June election, perhaps he could do something about reducing France’s structural government spending, while pursuing tax cuts and improved labor-market flexibility. Labor-market reform, in particular, could be crucial, not just for France itself, but also to convince German Chancellor Angela Merkel, if she is returned to power this September, to move toward greater fiscal integration, including the creation of a eurozone finance minister, which Macron advocates. Much of this is probably a long shot, but nowhere near as long as it was just a few months ago. And, given market valuations, it is much more interesting to explore such possibilities than it is to focus on many of the other issues that analysts obsess about.

Carrying the scenario further, one could even dream up an optimistic outlook for the UK’s trade balance, with a highly competitive exchange rate significantly improving demand in its major market, the eurozone. That could more than compensate for the challenges that arise from the end of single-market access. With this, the fantasy may have jumped the shark. But you never know.

The author is a former chairman of Goldman Sachs Asset Management and a former UK Treasury Minister

© 2017, Project Syndicate

www.project-syndicate.org

You May Like This

We are taking plagiarism seriously: TU Service Commission

KATHMANDU, August 3: Tribhuvan University Service Commission (TUSC), the staff recruiting body for the university, has taken the issue of... Read More...

Police not taking VAW cases seriously: Victims

RAUTAHAT, Feb 22: Thirty-five-year-old Champa Devi Bhagat of Matsari VDC-7 was thrashed by Rakesh Dhani of the same locality last Saturday.... Read More...

Government bodies not taking directives seriously: House committee

KATHMANDU, Dec 7: Parliamentary Development Committee has stated that the government bodies have not shown due seriousness toward implementing decisions and... Read More...

Ensuring Food Safety Amidst Challenges

21 hours ago

NRB unveils monetary policy

16 hours ago

NRB set to issue monetary policy today

18 hours ago

NEB to publish Grade 12 results next week

9 hours ago

NC defers its plan to join Koshi govt

10 hours ago

NRB to review microfinance loan interest rate

10 hours ago

Just In

- NRB to provide collateral-free loans to foreign employment seekers

- NEB to publish Grade 12 results next week

- Body handover begins; Relatives remain dissatisfied with insurance, compensation amount

- NC defers its plan to join Koshi govt

- NRB to review microfinance loan interest rate

- 134 dead in floods and landslides since onset of monsoon this year

- Mahakali Irrigation Project sees only 22 percent physical progress in 18 years

- Singapore now holds world's most powerful passport; Nepal stays at 98th

Leave A Comment