Saturday, 27 July 2024 10:14 AM

OR

Login using

Annual credit jumps 20.46% while deposit grows 17%

Published On: July 21, 2018 07:07 AM NPT By: Republica | @RepublicaNepal

Second consecutive fiscal year of the ultra-high interest rates

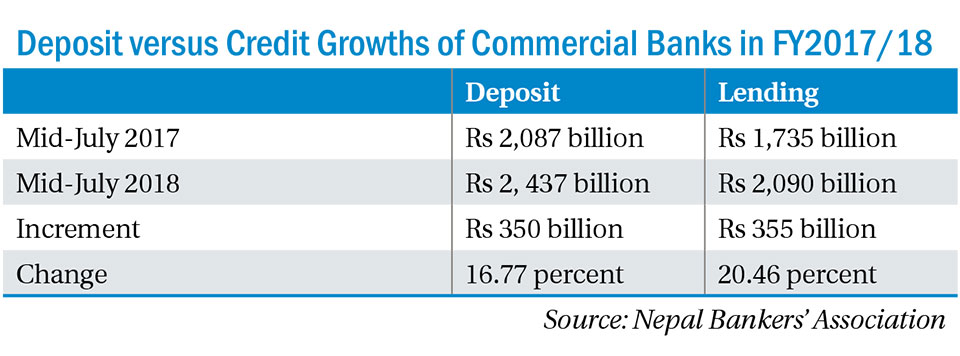

KATHMANDU, July 21: The banking industry continued to grapple with the mismatch of assets and liabilities in the last fiscal year as lending by commercial banks expanded 20.46 percent while their total deposits grew only 16.77 percent.

According to the data compiled by Nepal Bankers Association (NBA), 28 commercial banks’ total deposit rose by 16.77 percent, or Rs 350 billion, to Rs 2,437 billion in a year (between mid-July 2017 and mid-July 2018). On the other hand, their lending in the same period jumped by 20.46 percent, or Rs 355 billion, to Rs 2,090 billion.

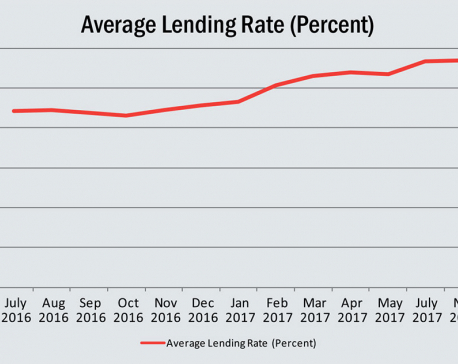

The credit expansion outpacing the deposit mobilization shows that the banks pursued an aggressive investment strategy in the last Fiscal Year 2017/18 despite scarce financial resources at their disposal. The mismatch between the lending and deposit growth has sent interest rates to an ultra-high level.

It was the second consecutive fiscal year of the ultra-high interest rates. Both deposit and lending rates have gone up during the past two years. The continuity of the spike in the interest rates could act as headwinds to economic growth of the country, warn economists.

Their lending climbed up to the level that the banks were forced to halt lending at one point due to the prudential lending limit of the Nepal Rastra Bank (NRB). The central bank has set 80 percent of credit to capital cum deposit ratio which means that a bank cannot lend more than 80 percent of what they have in deposit and core capital.

As the deposit growth could not keep up with the surge in the lending, banks were under immense pressure to raise interest rates to attract deposits. The increase on the deposit rate also prompted the rise on lending rate. While the fixed deposit rate rose up to 13 percent, some banks raised their lending rates up to 18 percent.

Fall in the remittance growth rate, slower capital expenditure of the government and rise of the import bill led to the slowdown in the deposit of banks. But, the lending increased rapidly on account of robust credit demands from the private sector and pressure on banks to ensure that returns to shareholders does not dwindle.

However, deposit growth has gathered strength following the rise in government expenditure and a slight improvement in the growth of remittances. The data shows that Rs 144 billion of deposits came in the last two months when the government boosted its development spending. During this period when banks focus on recovery rather than new investment, their lending grew by Rs 67 billion.

The central bank officials say that the growth in the deposit in the year end is helping stabilize market interest rates to some extent.

Amid growing concerns of skyrocketing interest rates resulting from the shortage of lendable fund, the central bank brought the monetary policy that is expected to augment loanable resources and lower interest rates in the long run. The central bank has lowered cash reserve ratio and statutory liquidity ratio, interest rate spread by 0.5 percentage point to 4.5 percent and increase in the size of refinance fund, among other host of measures.

You May Like This

Credit flow to service sector jumps 14 percent

KATHMANDU, April 29: Lending of bank and financial institutions (BFIs) to service industries jumped by 14 percent in the first eight... Read More...

Credit crunch bedevils banks: Bank deposit rate at 13%, lending rate spikes to 16%

KATHMANDU, Dec 29: Due to lack of farsightedness and aggressive lending practices among banks and financial institutions (BFIs), credit is... Read More...

Credit flow to service sector jumps 12 percent as tourism rebounds

KATHMANDU, March 15: In what appears to be an indication of the revival of service sector, credits from bank and financial... Read More...

NRB unveils monetary policy

20 hours ago

NRB set to issue monetary policy today

22 hours ago

Girl found unconscious at Gwarko guest house dies

23 hours ago

Nepal at high risk of Chandipura virus

9 minutes ago

Heavy rainfall likely in Bagmati and Sudurpaschim provinces

42 minutes ago

Bangladesh protest leaders taken from hospital by police

44 minutes ago

Challenges Confronting the New Coalition

1 hour ago

Just In

- Nepal at high risk of Chandipura virus

- Japanese envoy calls on Minister Bhattarai, discusses further enhancing exchange through education between Japan and Nepal

- Heavy rainfall likely in Bagmati and Sudurpaschim provinces

- Bangladesh protest leaders taken from hospital by police

- Challenges Confronting the New Coalition

- NRB introduces cautiously flexible measures to address ongoing slowdown in various economic sectors

- Forced Covid-19 cremations: is it too late for redemption?

- NRB to provide collateral-free loans to foreign employment seekers

Leave A Comment