Thursday, 25 April 2024 05:47 PM

OR

Login using

#Opinion

Nepal's Shrinking Revenue Collection

Published On: January 26, 2023 08:30 AM NPT By: Hari Prasad Shrestha

More from Author

- Why Federalism has Become Risky for Nepalese Democracy

- Hunger is a Serious Problem in South Asia

- Tourism Can Be A Catalyst For Change in Karnali Province

- Nepal’s Southern Border Has Become An Open Regional Crossroads

- Opening a new gateway for Kailash Mansarovar Yatra through Nepalgunj-GunshaNagari flight

Speaking at a program on the future of the economy that was organized by Nepal Chamber of Commerce (NCC) recently, Finance Minister Bishnu Paudel said that it is a matter of concern that the Nepali economy, which has overcome the Covid-19 pandemic and which even the earthquake could not bring down and which withstood the border blockade of 2015, is now in a state of downfall. The steepest decline in revenue collection in the past 48 years clearly indicates the downward trends of the economy.

Based on the statistics of the Office of the Comptroller General of Nepal, up to 2023/1/16 or the first six months of the current fiscal year 2022/23, the government has earned four trillion 95 billion rupees from revenue and grants and has spent five trillion 76 billion rupees. The expenditure is 81 billion rupees more than the income of the government. The operating expenses (current expenses) including administrative expenses alone are four trillion 55 billion rupees.

The blame for this huge loss in revenue collection, somehow goes to the effect of global recession and remains of Covid-19 as external factors. However, the internal factors are more responsible and to be blamed for the deteriorating revenue collections. These internal factors are: entry of inexperienced officers in the field; border smuggling and underground economy; evasion of customs duty, income tax, value added tax; tax exemptions in donor-assisted projects’ imported goods and the ban on the import of luxury goods.

The Ministry of Finance is at least as important, sensitive and equally significant as the Ministry of Foreign Affairs. Both of these ministries require highly-experienced, qualified, dedicated and cadre-based manpower with high moral support from the state for better international relations and economic stability. However, contrary to this, placing generalists at the field level under the Ministry of Finance without proper training and prior experience would certainly make it difficult for them to understand the entire revenue culture, unhindered revenue collection system and effective management of all stakeholders.

Based on a 2018 study by Medina and Schneider, the average value of Nepal’s shadow economy was at 37.5 percent of the total economy.

The next cause of decline in revenue is the illegal import of goods through the open borders as part of the shadow economy. During the unstable period of local and federal elections, people witnessed the illegal import of goods in unwarranted proportions. The unique open borders between Nepal and India that cannot be found elsewhere in the world coupled with the easy availability of the Indian currency has made it easy and comfortable for illegal imports and Nepal is losing billions of rupees in import duty and other taxes.

As the role of the shadow economy is the most dominating factor in the Nepali economy, based on a 2018 study by Medina and Schneider, the average value of Nepal’s shadow economy was at 37.5 percent of the total economy. The shadow economy constitutes unregistered economic activities that nevertheless play a part in the officially calculated Gross National Product. All activities that are of a criminal nature, including the trade of stolen goods, drug dealing and manufacturing, gambling, smuggling, and tax evasions go unreported, distorting the accuracy of key economic measurements, and thus affecting the GDP.

Every country in the world has a tax evasion problem - it is a global phenomenon. Studies suggest that 8eight percent of global financial wealth lies in offshore accounts. Often, offshore wealth that is stored in tax havens stays undetected in random audits. Even though there is high diversity among people who evade taxes, there is a higher probability among the highest wealth group. Many rich Nepalis are also linked with offshore wealth in tax havens.

In 2018, Nepal Rastra Bank (NRB), the country’s central bank, revealed a set of findings with serious implications. As per the NRB report, foreign direct investment (FDI) worth a total of Nrs 137.68 billion had been endowed to industries currently operating in Nepal. More than 60 percent of the FDI share, amounting to Nrs 82.65 billion, came from tax haven countries, of which only 17 have been approved to invest by the Nepal government, according to the report. Investments from the British Virgin Islands and nearby countries in the Caribbean alone comprise Nrs 62.78 billion.

Customs duties are the most important source of revenue and some importers try to evade customs duty by under-invoicing and by misdeclaration of quantity and product-description. When there is ad valorem import duty, the tax base can be reduced through under-invoicing. Misdeclaration of quantity is more relevant for products with specific duty. Production description is changed to match a Harmonized System (H.S.) Code commensurate with a lower rate of duty.

Income tax evasion often involves the deliberate misrepresentation of the taxpayer's affairs to the tax authorities to reduce the taxpayer's tax liability through tax avoidance, and it includes dishonest tax reporting, declaring less income, profits or gains than the amounts actually earned, overstating deductions, using illegal methods to influence authorities and by hiding undeclared money in secret locations or tax haven countries. In case of VAT, the sellers who collect VAT from consumers may evade tax by under-reporting the amount of sales.

Exemptions of customs duty and other taxes on the import of project materials are also causing a deficit in revenue collection in Nepal. The sphere of duty exemption is so vague that it is not certain which project on what quantity would get tax exemptions in the import of materials. Except otherwise specified by the Vienna Convention on Diplomatic Relations of 1961 treaty, other numerous tax exemptions are provided, under project agreements on the import of goods in Nepal.

For example, the Government of Nepal may accord partial or full customs duty exemption to the goods to be imported in the name of any project to be operated under foreign loan or grant assistance or in the name of the contractor of such a project; this vague provision of tax exemption is causing a huge loss in government revenue collection.

The temporary ban on the import of some luxury items also affected the revenue collection. The government banned the import of goods in order to improve the foreign exchange reserves. Many countries are struggling to collect sufficient revenues to finance their own development. Countries collecting less than 15 percent of GDP in taxes must increase their revenue collection. This level of taxation is an important tipping point to make a state viable and put it on a path to growth. Previously, Nepal was above this ratio in revenue collection, which went down.

Nepal needs fairness in its tax system and equality in policy support to all. There is a need to ensure that the tax system is fair and equitable. Fairness considerations include the relative taxation of the poor and the rich; corporate and individual taxpayers; cities and rural areas; formal and informal sectors, labor and investment income; and the older and the younger generations.

Nepal Rastra Bank has removed the provision of cash margin for the import of some luxury items and the government has also lifted the ban on all items previously restricted for import. It would contribute to the revenue collection to some extent.

The level of evasion of taxes and duties depends on the detection probability, regular market inspection, MRP compulsion with company name on each imported item and the level of punishment provided by law. Individuals are also more likely to comply with taxes when they believe that tax money is appropriately used and when they can take part in public decisions.

Moreover, reducing high tax rates and making more simplified laws and simplified systems with a well-organized tax administration structure of well experienced capable manpower would be supportive for better accomplishments in revenue collections.

You May Like This

NRB tightens restriction on lending for senior management officials

KATHMANDU, Sept 10: Nepal Rastra Bank (NRB) has tightened loans that bank and financial institutions (BFIs) floated to their senior... Read More...

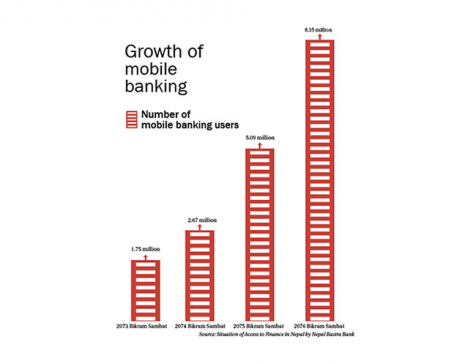

Mobile banking users increase by over 4.5 times in 4 years

KATHMANDU, Oct 24: The number of mobile banking users has increased by over 4.5 times in the past four years.... Read More...

NRB directs banks to ease concessional loans

KATHMANDU, Jan 31: Following complaints that bank and financial institutions (BFIs) were reluctant to provide concessional loans under the government... Read More...

Karnali CM Kandel secures vote of confidence

20 minutes ago

Just In

- Karnali CM Kandel secures vote of confidence

- National Youth Scientists Conference to be organized in Surkhet

- Rautahat traders call for extended night market hours amid summer heat

- Resignation of JSP minister rejected in Lumbini province

- Russia warns NATO nuclear facilities in Poland could become military target

- 16th Five Year Plan: Govt unveils 40 goals for prosperity (with full list)

- SC hearing on fake Bhutanese refugees case involving ex-deputy PM Rayamajhi today

- Clash erupts between police and agitating locals in Dhanusha, nine tear gas shells fired

Leave A Comment