Thursday, 25 April 2024 09:32 PM

OR

Login using

Monetary Policy a mixed bag for pvt sector

Published On: July 13, 2018 07:10 AM NPT By: Republica | @RepublicaNepal

KATHMANDU, July 13: Nepal Rastra Bank (NRB) introduced Monetary Policy for Fiscal Year 2018/19 in Kathmandu on Wednesday. The monetary policy unveiled a week before the new fiscal year begins has drawn positive responses from bankers, business leaders and economic analysts, as it focuses on reining in the runaway interest rates that has dampened confidence of the private sector which was increasingly finding credit from the banking industry unaffordable.

Republica talked to leaders of private sector and bankers to get their views on the monetary policy. Excerpts:

No surprises

Anil Keshary Shah, CEO, Nabil Bank Ltd

The new monetary policy is a mixed bag for me. Reduction of cash reserve ratio, non-requirement of CRR for branch offices in rural areas and the provision of allowing brokerage business for banks through a subsidiary are some of the positive aspects of the monetary policy. The stock market will now not only be for the people inside the Ring Road, but for all Nepali people. On the other hand, the central bank has brought down the interest spread rate to 4.5 percent which we have not taken very well. Overall, I am very happy with the monetary policy because there are no surprises in it. There are no forceful merger announcements. Shortage of lendable fund has been addressed only by increasing the government spending. The biggest source of liquidity for banks is the government. If the government actually spends the budget from the first day of the new fiscal year, there is a very good chance that the budget would be fully implemented and monetary policy would be successful. The monetary policy is a start toward reducing sky-high interest rates. However, the interest rate volatility largely depends on how well the budget is implemented.

Personal overdraft limit should be reviewed

Analraj Bhattarai, President, Finance and Monetary Policies Committee of CNI

The reduction of CRR and SLR will help to bring down the base rate of banks which will eventually help to curb rising lending rates. Similarly, the decision to lower interest spread to 4.5 percent from existing 5 percent is also a positive move. For me, the monetary policy looks balanced. Also, the central bank is allowing calculating the borrowing of banks in credit to core capital cum deposit (CCD) ratio. Now it would be like CCDB ratio as banks will be able to include the borrowing they make for the purpose of calculating this ratio. This will increase lending capacity of banks to some extent. However, tightening of personal overdraft may hit small and micro enterprises who have been relying for such loans as they cannot get structural loans. The central bank should review this new limit. As our economy is import-based economy, huge amount of credit also gets channelized for the trading purpose. However, it remains to be seen how the government spending pattern will go and whether there would be adequate lendable fund in the banking system.

Our demands have been addressed

Saroj Kaji Tuladhar, President, Nepal Financial Institutions Association

We had been requesting the central bank to ensure representation of development banks and finance companies in grievance hearing unit of the NRB. The demand has been addressed this time. Until last year, BFIs could bid deposits from the institutional depositors at 2 percent higher than the published rate. This has been reduced to 1 percent now. This will help to check the interest rate war in the market. Regarding margin lending, there used to be a cushion of 10 percent which has now been increased to 20 percent. The increase in the cushion will end the compulsion of forceful selling of shares due to margin and selling pressure in the stock market. We can expect some stability in the stock market due to this new provision. However, the whole capacity of bank and financial institutions to extend loans in the stock market has been reduced to 25 percent of the core capital of BFIs from existing 40 percent. The tightening of margin type of exposure will shrink financial resources to the stock market. Another positive aspect of the monetary policy for finance companies is that we will also be able to mobilize subordinate capital by through instruments like bonds and debentures.

Private sector is positive

Shekhar Golchha, Senior Vice President, Federation of Nepalese Chambers of Commerce and Industry

The size of refinance fund has been increased to Rs 35 billion. This is a welcome move. However, our demand to also increase the maturity period has not been addressed. We request the central bank to increase the maturity period as well and expand the sectors that benefit from this concessional lending facility. The average interest spread has been reduced which we expect to rein in skyrocketing interest rates. But, we still see the need to bring down the interest rate spread by one or two percentage points. We are also upbeat with the central bank’s decision to allow banks to borrow in Indian currency along with other convertible currencies. This will help to address the recurring shortage of lendable fund in the banking system. The provision to slash cash reserve ratio and statutory liquidity ratio will also free up more funds and ease liquidity. This monetary policy provides some relief to private sector which has been suffering from ultra-high and unpredictable lending rates. However, we are worried that inflation in the upcoming fiscal year is likely to rise on account of minimum wage growth and the decision to raise tax rates.

You May Like This

Monetary policy draws mixed reaction

KATHMANDU, July 9: Representatives from business associations, including Nepal Bankers' Association, and Federation of Nepalese Chamber of Commerce and Industries... Read More...

NRB to unveil monetary policy next week

KATHMANDU, June 27: Nepal Rastra Bank (NRB) is preparing to unveil monetary policy for the upcoming fiscal year next week. According... Read More...

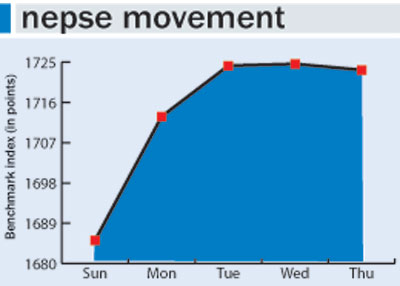

Nepse down 3 points as investors await monetary policy

KATHMANDU, July 9: Nepal Stock Exchange (Nepse) index shed 3.48 points this week to close at 1,715.72 points on Wednesday... Read More...

Karnali CM Kandel secures vote of confidence

4 hours ago

Just In

- World Malaria Day: Foreign returnees more susceptible to the vector-borne disease

- MoEST seeks EC’s help in identifying teachers linked to political parties

- 70 community and national forests affected by fire in Parbat till Wednesday

- NEPSE loses 3.24 points, while daily turnover inclines to Rs 2.36 billion

- Pak Embassy awards scholarships to 180 Nepali students

- President Paudel approves mobilization of army personnel for by-elections security

- Bhajang and Ilam by-elections: 69 polling stations classified as ‘highly sensitive’

- Karnali CM Kandel secures vote of confidence

Leave A Comment