Thursday, 25 April 2024 05:10 PM

OR

Login using

More from Author

The focus of development planning has shifted from economic growth to reducing inequality. Economic growth alone, as we have seen, has not been able to reduce poverty and inequality in developing economies. The assumption that the benefits of economic growth would eventually “trickle down” to lower segments of the society and thus correct the inequality proved inadequate in many countries. This led to more pro-poor and inclusive development planning, in order to create economic opportunities and enhance poor people’s access to financial services.

The UN’s declaration of year 2005 as the international year of micro-credit; the involvement of G20 and other international agencies in financial inclusion and poverty alleviation; the IMF-World Bank’s 2015 commitment for universal financial access by 2020; establishment of organizations such as the Alliance for Financial Inclusion (AFI) and the Consultative Group to Assist the Poor (CGAP); eradication of poverty and hunger in line with the Millennium Development Goals (MDGs)—these are all indications of the seriousness with which inclusive growth is being pursued.

Microfinance in particular refers to poverty-focused programs that provide financial and business services to very poor people for their greater involvement in self-employment and income-generation activities. It is an important means of breaking the vicious circle of poverty and lifting the economic status of the poor. Microfinance offers banking services to the poor and creates business opportunities to use their assets well. It also helps generate income by creating new jobs, developing new products and services and infrastructure-building. It creates an inclusive business model for the poor to work as employees, entrepreneurs, suppliers, distributors and customers. Microfinance also helps with financial literacy, awareness and consumer protection.

Microfinance is not a choice but a necessity for Nepal as around 80 percent of our population lives in rural areas. Around 25 percent Nepalis are still below the UN-set US $1.25 poverty line and two-thirds of the population is dependent on agriculture. Added to poor infrastructure development, low financial literacy, limited economic opportunities in rural areas and increasing urbanization and migration, the pathway to economic development in Nepal has to be pro-poor and inclusive growth. Moreover, the demand-side study conducted by Nepal Rastra Bank (NRB) revealed that only 40 percent of adult population in Nepal is ‘banked’, 61 percent is financially served, 57 percent is informally served and 18 percent is financially excluded. Around 57 percent adults have deposit accounts and 46 percent have borrowed money. This shows that financial services are yet to reach most of the rural people and so unlocking their savings and credit behavior is a major challenge in Nepal.

Structurally, commercial banks, development banks, finance companies, micro-credit development banks, cooperatives and non-governmental (intermediary) organizations are involved in delivering financial services in Nepal. However, creating business opportunities for most-vulnerable rural people has largely been left to micro-finance institutions (MFIs). MFIs have been instrumental in identifying financial needs of the most vulnerable poor people, encouraging them to start income-generating activities, promoting group-based lending without collateral and creating awareness on banking and offering banking services. That is not all. Microfinance has also been successful in empowering women, developing confidence among banks and financial institutions (BFIS) that poor people are bankable, raising social cohesion, and, ultimately, reducing poverty. MFIs have taken their services to the doorsteps of rural people in all 75 districts and generated employment for thousands of poor people.

Nepal Rastra Bank has taken many policy measures to avail financial services in remote areas. For instance, commercial banks, development banks and finance companies are required to provide 5 percent, 4.5 percent and 4.0 percent of total credit to deprived sectors respectively. New licenses for microfinance institutions are being given. Moreover, BFIs must establish rural branches first to be eligible to establish branches in urban areas. Interest-free loan is provided to help BFIs to expand into remote districts.

The central bank also provides special refinance facility to BFIs to lend to small and cottage industries and enterprises run by women. Financial Literacy Policy targeted at rural people is in the process of approval. Lastly, MFIs are mandatorily required to allocate funds from their profit for consumer protection and education.

Despite these efforts, there are still many challenges, both from demand and supply sides. The wide geographical dispersal of our population,

poor infrastructure, documentation hurdles and high cost of financial services are some of these challenges. To compound things, the regulations governing microfinance are opaque which is perhaps why there is absence of banking products tailored to the needs of the poor people.

Likewise, supply-side constraints include reluctance of large banks to expand into rural areas, the question of financial viability of operating in rural areas, perceived risks in micro-lending, high cost of maintaining rural branches and low economic activities in rural areas.

Microfinance is one of the best gateways for inclusive growth in Nepal. International experience shows that microfinance can create plenty of economic opportunities for uplift of the poor. But there is a need to bring more of the poor people into banking and encourage micro-savings.

Savings in turn encourage individuals to invest. But most rural people still find it easier to deal with informal markets due to ease of access and easy documentation. Therefore, regulatory norms for small savings and credit need to be simplified in order to attract more rural folks into the formal financial system. The poor are financially vulnerable, especially after natural calamities. But insurance for micro-businesses is among the least-developed financial products in Nepal and when available, it’s expensive.

Addressing these issues is important for inclusive growth in Nepal. Technological advancement means reaching the poor people is neither expensive nor time-consuming. Therefore it is about time both regulators and private actors thought of ways to use technology to improve financial delivery channels in Nepal. In the end, I would like to reiterate the importance of public-private collaboration to strengthen microfinance and take the country on a path of sustainable and inclusive growth.

The author is an Executive Director at Nepal Rastra Bank and oversees its Micro-Finance Promotion & Supervision Department

binodatreya@hotmail.com

You May Like This

Global IME Bank starts 46th branchless banking unit

KATHMANDU, May 24: Global IME Bank has started providing branchless banking service in Kalikot district. ... Read More...

Banking stakeholders discuss cyber threats

KATHMANDU, Dec 17: Nepal Bankers' Association (NBA), in association with Microsoft, on Friday organized a gathering of banking and financial services... Read More...

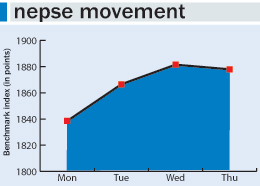

Nepse up 79 points as investors turn to banking stocks

KATHMANDU, July 30: Nepal Stock Exchange (Nepse) index gained 79.1 points this week to close at 1,881.45 points on Thursday--the... Read More...

Forest fire destroys 13 houses in Khotang

3 hours ago

Just In

- Rautahat traders call for extended night market hours amid summer heat

- Resignation of JSP minister rejected in Lumbini province

- Russia warns NATO nuclear facilities in Poland could become military target

- 16th Five Year Plan: Govt unveils 40 goals for prosperity (with full list)

- SC hearing on fake Bhutanese refugees case involving ex-deputy PM Rayamajhi today

- Clash erupts between police and agitating locals in Dhanusha, nine tear gas shells fired

- Abducted Mishra rescued after eight hours, six arrested

- Forest fire destroys 13 houses in Khotang

Leave A Comment